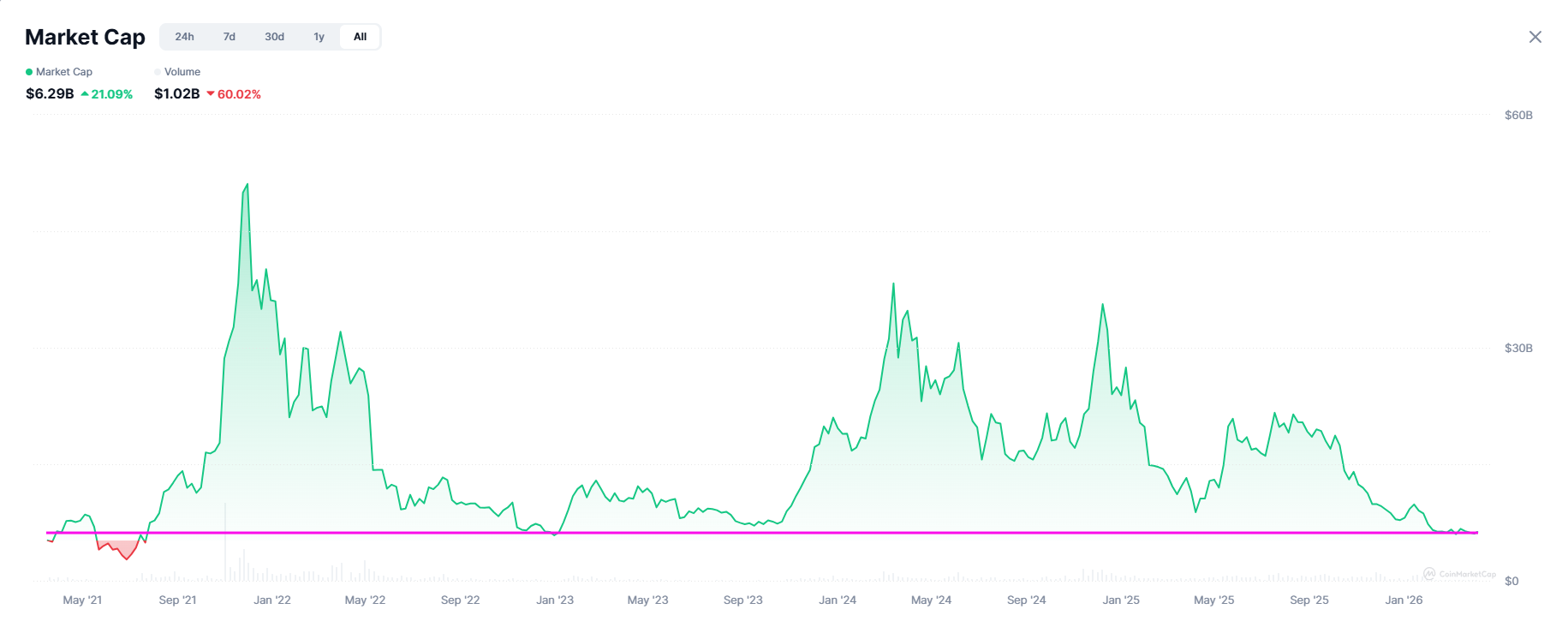

We’ve entered the bear market. Your portfolio is in shambles, and it’s not only your (“worthless”) altcoins that are suffering. Your majors are too. Gaming isn’t exempt from this massacre, as the total market cap of gaming (according to CMC) has nearly reached the bottom of 2023 of ~$5.9B in January. In comparison, the total market cap of crypto since then is up roughly 2.8x.

With that in mind, it’s time again for another update on what new tokens have popped up recently, specifically in Q1 2026. The goal is to get an overview of what tokens have launched, how they have performed, and what we can learn from the data.

For reference, we will use some of the 2025 EOY token data shared in Sidelined Alpha 79 (December 2025). Do note that the price data has been updated to make an accurate comparison for the new TGEs in 2026.

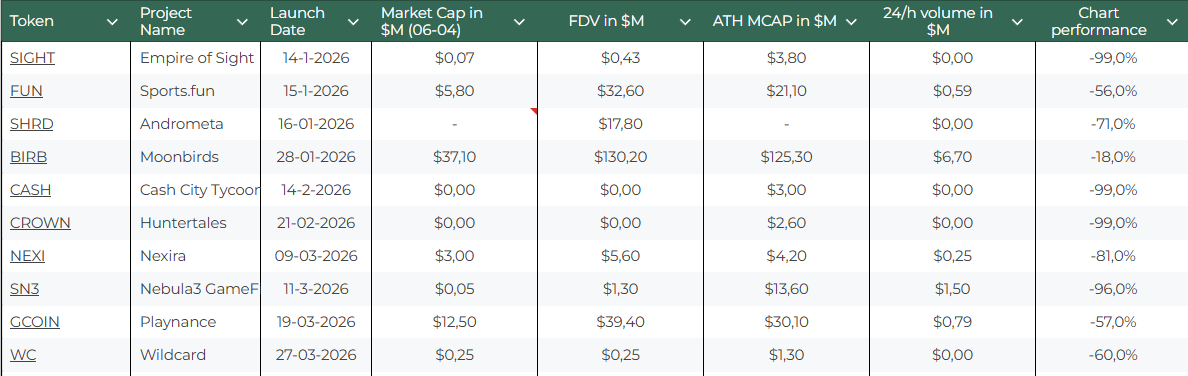

As you can see, the number of TGEs in Q1 2026 is low, with only 10 new launches. Because of the size of the sample, the findings might be surprising (skewed) in comparison to 2025, but it’s also telling of the reality of the market.

Overview of the data:

Number of Launches

As said, there were a mere 10 launches (N) in Q1 2026. In comparison, we had over 2x as many N in Q1 2025, with 23 new tokens. However, we’ve seen an ongoing downtrend of N from Q3 (N=28) to Q4 2025 (N=17), and Dec 2025 (N=3) specifically, as a result of the worsening market sentiment and conditions.

Furthermore, using the data from 2024, we can get a broader picture of how N is slowing down:

2024: (N=100) | Q1 (N=19)

2025: (N=87) + Q1 (N=23).

2026: (N=?) + Q1 (N=10)

Average Performance

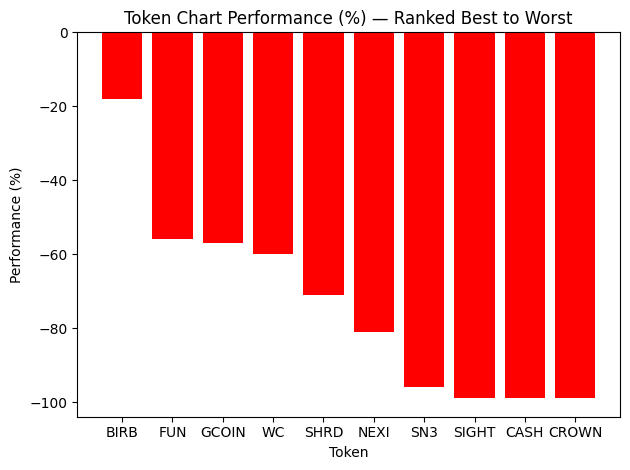

The average performance of gaming TGEs in 2026 is -73.6%. This is based on the opening price of the tokens according to CMC, Coingecko, and DEXScreener. So, do note that these differ from token listing prices (in the case of listings on CEXes).

Previously, I have used X-day market cap/market cap ATH to measure performance. However, the above measurement is a more accurate presentation.

Nonetheless, the numbers are similar, as the average drawdown of all TGEs in 2025 today is -80.5% (based on the old methodology). Do note that over time, a dozen or so tokens have been deprecated (e.g., listing has been removed). Moreover, a significant number of tokens have close to zero volume and so retain their value, because nobody is either buying or selling.

The largest enemy of these token charts? It remains to be time.

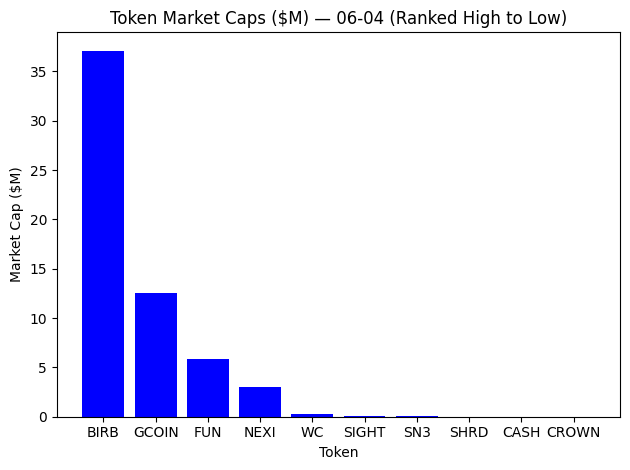

Average Market Cap

The average market cap of Q1 2026 TGEs is a mere $6.5M. This number is also inflated by Moonbird’s BIRB token launch, which is more of a “brand token” than a gaming token, yet should be included in this list, due to its business in gaming. When excluding BIRB, the average market cap is $2.4M (-63%).

The average market cap at the EOY for all TGEs in 2025 came out to be $19.6M. Today, that number has shrunk to $11.5M (-41%). Excluding the top 5 tokens (by MC), that number further shrinks to $3.4M (-70%). In combination with the median only being $0.47M, it illustrates how top-heavy the distribution of tokens is.

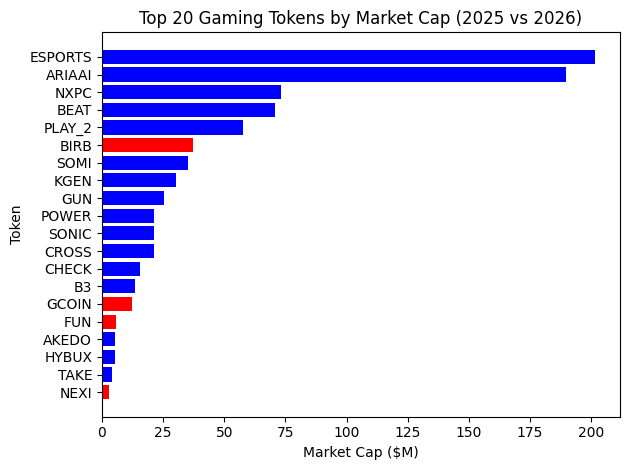

Top 20 Tokens by MC

After merging the 2025 TGEs with 2026 and only displaying the top 20 tokens by MC, we get the following overview (2025 = blue, 2026 = red):

The bar chart shows the dominance of tokens that were minted in 2025 compared to 2026. Thus far, 2026 seems to be underperforming in creating new “winners”, but considering the bearish market conditions, that isn’t surprising.

Larger projects in terms of revenue, investments, and users (e.g., OpenSea) are also often more hesitant to launch in bearish conditions, because they want/need a higher opening valuation. Of course, this is much more difficult to achieve in bearish than in bullish market conditions.

Average 24H Volume

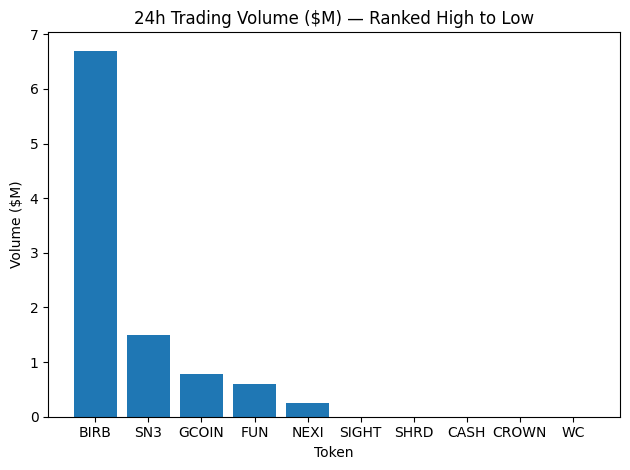

The average 24h volume of new tokens is $0.98M. As shown in the chart below, volume is dominated by BIRB. When excluding BIRB, the average becomes $0.35M (-64%). Notably, 5/10 tokens on this list have less than $1,000 in 24h volume. These include a combination of projects that already failed (e.g., CASH and CROWN) or completely flopped (e.g., WC).

Unfortunately, the average volume for gaming TGEs in 2025 isn’t (and wasn’t) looking great either. At the EOY, the average was $14.9M, but today it’s only $1.9M (-87%). It’s important to add here that these numbers were heavily skewed by the outliers, as by excluding the top 5, the respective 2025 numbers are $1.34M (at EOY) and $0.85M (today).

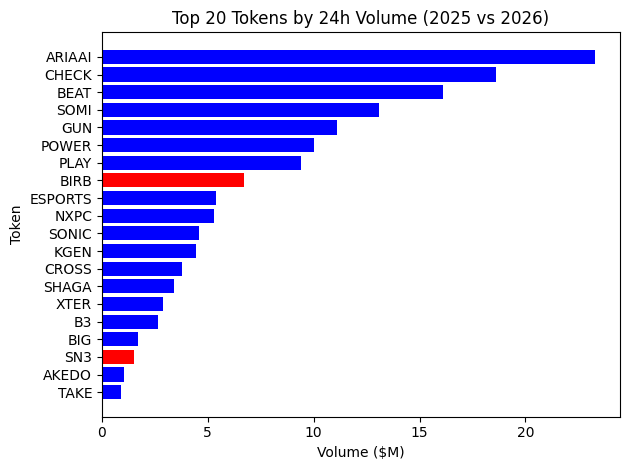

Top 20 tokens by Volume

We can merge the 2025 and Q1 2026 data and get an overview of the top 20 tokens by volume (2025 = blue, 2026 = red):

Despite the lower number of new launches (i.e., less competition), new tokens still struggle to attract liquidity. Likely, both a result of the lack of liquidity in the market right now, and the lack of appetite for (new) alts, including gaming tokens.

Conclusion

Based on the data, we can make the following conclusions:

The market cap of gaming continues to shrink

New TGEs slowed down due to worsening market sentiment

Time remains the worst enemy of any token

2026 isn’t creating new “winners” thus far

Trading volume is a better indicator of reality than market caps

Trading volume is down as a result of less liquidity and a lack of appetite for alts, including gaming

Overall, it’s a bunch of “doom and gloom” (like usual…), and I believe not only the market environment, but a handful of other factors and trends will slow down the number of new TGEs this year.

The Slowdown of Tokens

In 2024, we saw 100 new gaming tokens. In 2025, there were 89, and in 2026, I think there will be fewer than 50. This development will be multifactorial:

The first reason is the most obvious one: there will be fewer games that’ll launch in the first place. Over the past two years, much of crypto gaming’s “dead weight” has been shed through failures. And there are simply not that many teams left developing games that have yet to launch a token.

The “TGE massacre”, as laid out in the previous sections, will start to make more teams reconsider whether they need a token or can adopt stablecoins instead. Or at least, makes teams battletest their systems with a stablecoin before introducing their own token.

On a similar topic, I foresee more teams adopting “game-branded stablecoins”, like Gigaverse’s GIGABIT and Apptokens (like bAXS) to gain greater control of the in- and outflows of a token. This will lead to a decrease in traditional (utility) token launches.

Another development that I believe will lead to less traditional token launches and larger stablecoin adoption is the increasing need to go after audiences outside of crypto. For these audiences, playing to earn a “digital dollar” (e.g., USDC) makes much more sense than playing to earn tokens named after tickers they’re not familiar with.

Lastly, there will be consolidation, as the larger gaming companies (with sizeable treasuries) will seek other builders to build in their ecosystem, on their infrastructure, in an attempt to revitalize their tokens, e.g., Pixels and Stacked. This means more games will integrate existing tokens, and fewer will launch their own.

Overall, token fatigue has peaked, so I see fewer new tokens being launched as a net benefit, instead of an indicator that the space is dying.

Disclaimer: None of this information should be taken as financial advice. My writings only represent my personal opinions. DYOR. I will hold some of the assets mentioned in this newsletter.